DocuSign's Earnings Overview

Another stellar quarter

DocuSign’s ($DOCU) earnings for Q1 2022 (the company’s fiscal year is one ahead of the calendar year) came out two weeks ago, on Thursday the 3rd of June, and they were…

The growth story for the company remains intact post-COVID as management has always said and the execution looks flawless. In this article I will give an overview of these earnings as well as a brief overview of the company just in case you are not familiar with it or you forgot a bit about it.

What DocuSign does

Many people identify DocuSign as an eSignature company and, even though this is a good approximation, it ignores most of the company’s potential going forward: the Agreement Cloud.

Before digging deeper into the company I thought that the company had no moat and that their product could be easily replaced by another solution such as the one Adobe ($ADBE) offers. Once I discovered and learned about the Agreement Cloud my views changed and know I understand the true potential of the company.

DocuSign is a company that aims to digitize the whole agreement process, not just the signature phase. The Agreement Cloud offers several advantages with respect to traditional paper based processes:

Eliminates the use of paper

Automates the whole agreement process

Enables connection with many of the customer’s systems such as Salesforce, Microsoft, SAP…

Allows the customer to keep logs of changes made to the documents throughout the process

Reduces human errors

…

What is the Agreement Cloud exactly? The Agreement Cloud aims to digitize the whole agreement process and has 4 distinguished phases: Prepare, Sign, Act and Manage. I will simply bring here the company’s definition for these phases because I don’t think I would be able to explain them any better:

Prepare: activities that aim to create an agreement to the point that it is ready for signing

Sign: activities that aim to get the signature executed in a legally valid manner

Act: activities that aim to fulfill the signed agreement’s terms. For example, if the agreement requires a payment this amount can be automatically transferred to a billing system

Manage: activities that aim to manage agreements that have already been completed

Source (DocuSign)

In the source above you can find a full PDF of the company about The Agreement Cloud.

So basically investors who think that DocuSign is simply an eSignature company are just looking at point 2 and completely ignoring point 1, 3 and 4.

The opportunity ahead

How big is the opportunity for the company? The company estimates its TAM to be $50 billion, which they equally divide between the signature phase and the rest of the phases:

Source (DocuSign Quarterly Presentation)

eSignature is a very important component of the company’s opportunity because it serves as the entry point of their land-and-expand model. Once the company has sold this solution their objective is to upsell the rest of the agreement cloud which is the really sticky product.

Currently, most of the company’s top line is made up of revenues generated by the eSignature solution and the company does not expect to see a meaningful contribution of the Agreement Cloud to the top line in the short term:

“And when you think about kind of the results that we posted the last few quarters, they are primarily driven by eSignature. And just given the scale and the growth rate kind of on the core piece, it’s going to take a while for Agreement Cloud, even if it’s growing quickly within to really have be a meaningful contributor from a top-line perspective.”

Source: Q12022 Earnings Transcript

DocuSign is expected to generate revenues of $2.03 billion this year which means that the company would be just above 4% of Total Addressable Market (TAM). CEO Dan Springer said the following:

So, the TAM, we are still in the early days, even of just with eSignature business, our penetration is so low, but it’s a very, very large ocean from which we’re pulling forward that continued strong customer demand. So that’s how we look at it. I think it’s fairly straightforward.

Source: Q12022 Earnings Transcript

Of course, this huge TAM can’t come for free, competition is expected to be intense. Companies such as Adobe are also working on a similar end-to-end (E2E) solution but DocuSign has several advantages that make me remain optimistic about their leadership going forward:

DocuSign is the indisputable market leader in the eSignature space with a market share of approximately 70% with Adobe coming second with a market share of 20%. This is very important because, as I mentioned above, this offering is the entry point to the agreement cloud for most customers.

The company has a first mover advantage with the Agreement Cloud although they have to execute flawlessly to upsell this integral solution across its existing customers. DocuSign’s large customer base will surely help the company with product adoption going forward.

Q1 2022 Earnings Report

Once we have briefly discussed what the company does and the opportunity ahead, it’s time to look in-depth at the first-quarter earnings report. It’s very important that for this part you remember that Q1 2022 is the most recent quarter and Q1 2021 is last year’s comparable period because the company’s Fiscal Year is one year ahead of calendar (Fiscal Year 2022 started the 1st of February 2021).

I will first give an overview of the most important highlights and then I will discuss the most important KPIs for the company in detail.

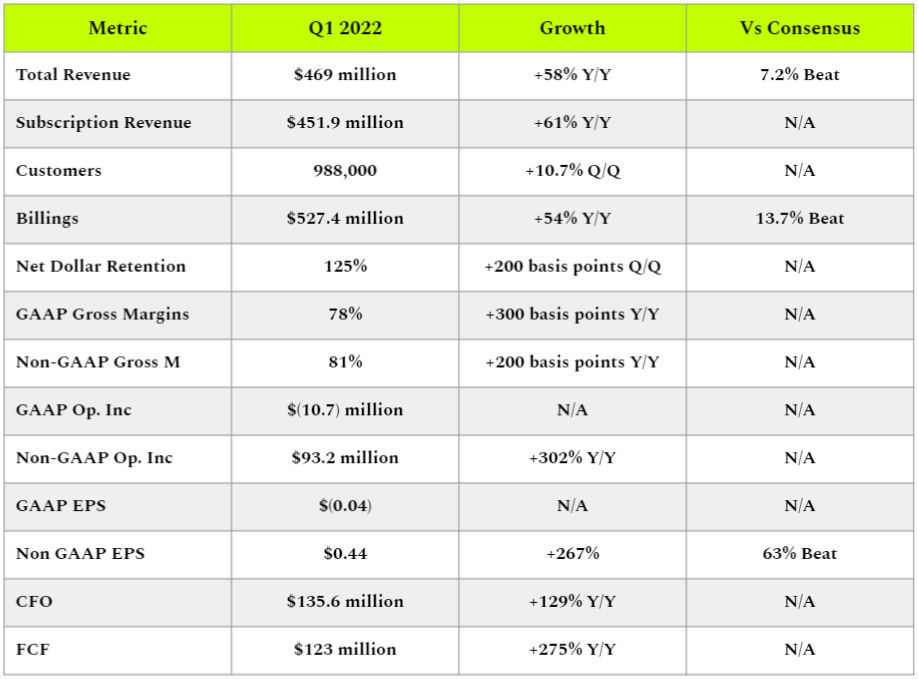

Earnings Highlights

Total revenue of $469.1 million, an increase of 58% Y/Y. The consensus was $437.66 million (+47.4% Y/Y). 7.2% BEAT

International revenue of $101 million, an increase of 84% Y/Y. International revenue made 21% of total revenue

Subscription revenue of $451.9 million, an increase of 61% Y/Y

The company acquired 96,000 new customers in the quarter, an increase of 10.7% sequentially (Q/Q). Total customers for the company stood at 988,000 at quarter end

11,000 new enterprise and commercial customers, an increase of 8.8% sequentially (Q/Q). Enterprise and commercial customers stood at 136,000 at quarter end

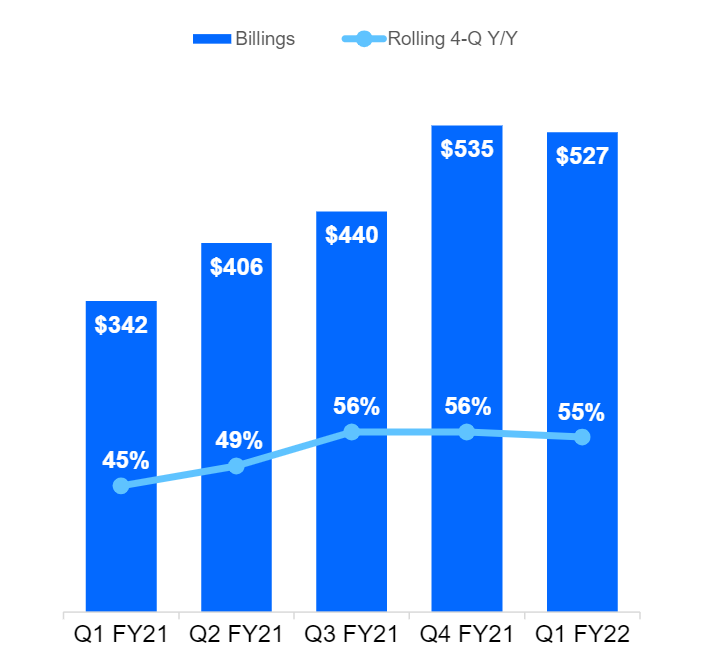

Billings were $527.4 million, an increase of 54% Y/Y. Analysts expected billings of $463.9 million. 13.7% BEAT

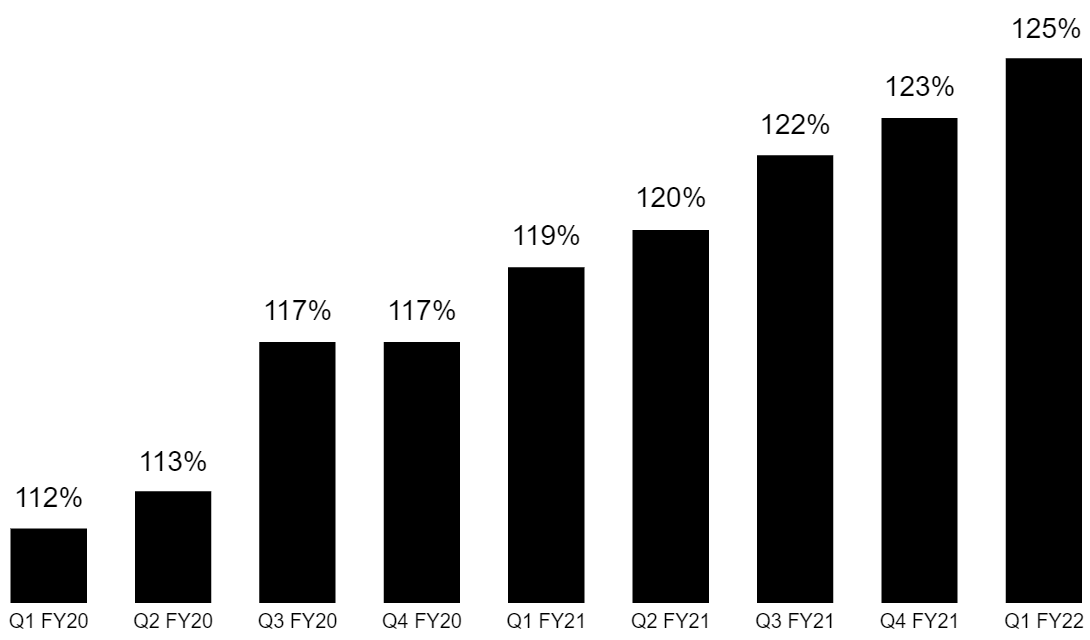

Net Dollar Retention stood at 125%, an improvement of 200 basis points sequentially.

GAAP Gross Margin was 78%, up from 75% in Q1 2021. Non-GAAP Gross Margin was 81%, up from 79% in Q1 2021

Non-GAAP Operating income of $93.2 million, an increase of 302% Y/Y. Non-GAAP Operating Margin for the quarter was 20%

GAAP EPS came at a $(0.04) loss which was an improvement with respect to the comparable quarter $(0.26)

Non-GAAP EPS came at $0.44, an increase of 267% Y/Y. Consensus was $0.27. 63.7% BEAT

Cash Flow from Operations (CFO) was $135.6 million, an increase of 129% Y/Y. CFO margin for the quarter was 28.9%.

Free Cash Flow was $123 million, an increase of 275% Y/Y. FCF margin for the quarter was 26.2%

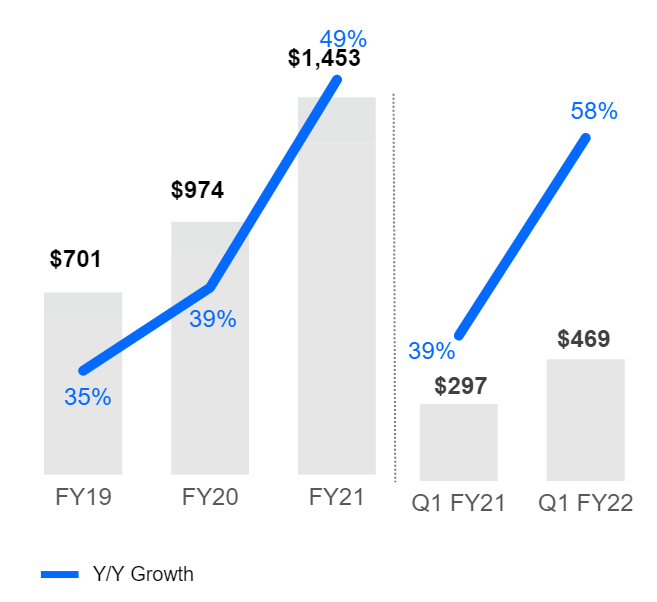

Revenue

Total revenue for the quarter grew a whopping 58% Y/Y which is the highest revenue growth that the company has achieved since the pandemic started. This probably hurt the feelings of those bears that thought of DocuSign as a COVID play…

Source: DocuSign’s Quarterly Earnings Presentation

Taking a look at the geographical distribution of revenue, international revenue made up 21% of total revenue and reached $101 million in the quarter, an increase of 84% Y/Y. This is the first time that international revenue is above $100 million in any given quarter.

During the earnings call, management said that international markets continue to be the biggest future growth driver for DocuSign and the largest part of the company’s TAM so it’s great to see that this segment is growing fast.

According to management, international markets are in a similar stage than domestic markets were a couple of years ago but the international segment is growing at a pace never seen before in the domestic segment. This shows that management has perfectly applied the lessons it learned while growing domestically and improved their strategy to apply it internationally.

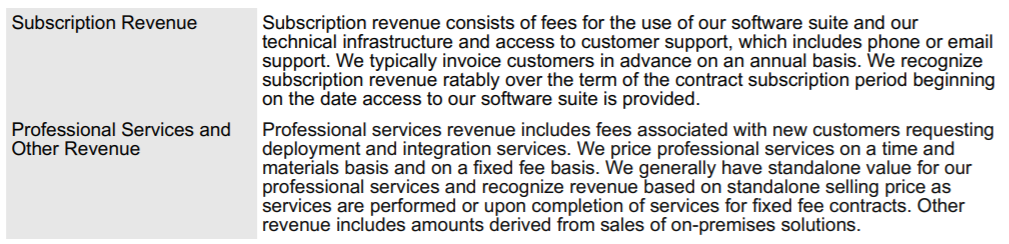

Another important thing to take into account is revenue distribution. DocuSign generates revenue from two main sources:

Source: 10K Report

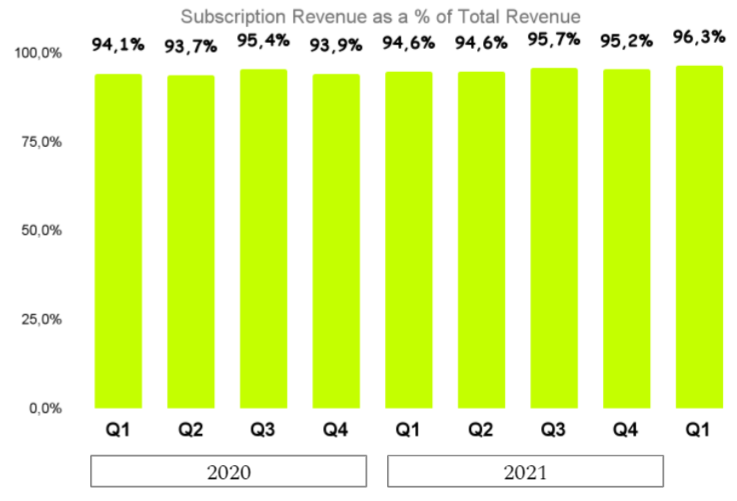

We could simplify by saying that subscription revenue is recurrent while the rest is one-time. Any investor would like to see high subscription revenue as a percentage of total revenue. Well, I have good news, this is definitely the case for DocuSign:

Source: Quarterly Earnings Presentations

Subscription revenue as a percentage of total revenue stood at 96.3% for the quarter, an increase of 170 basis points Y/Y. Subscription revenue for the quarter stood at $451.9 million, an increase of 61% Y/Y.

Overall, the company showed strong top line growth, demonstrating once more that it is not a COVID play. International revenue is growing very fast and most of the revenue is recurring.

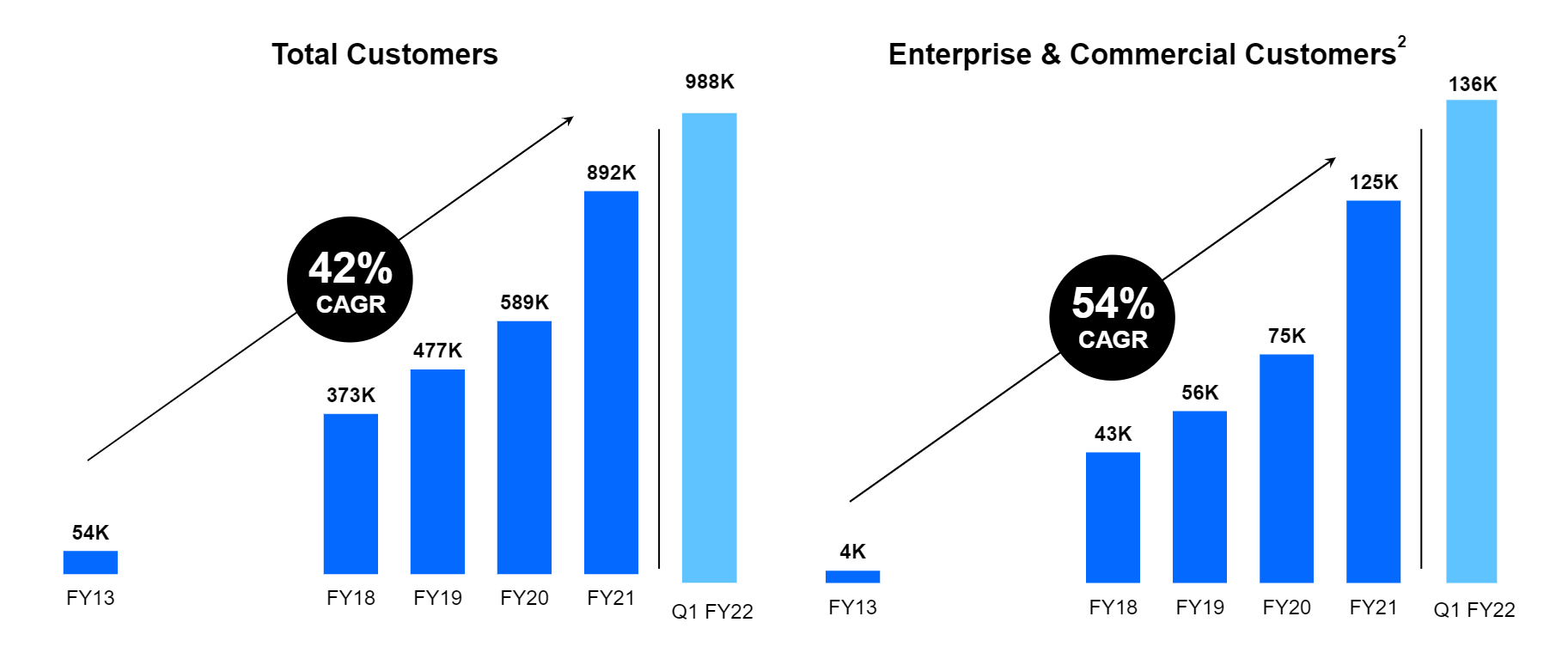

Customers

The company added 96,000 total customers in the quarter from which 11,000 where Enterprise and Commercial customers:

Source: DocuSign’s Quarterly Earnings Presentation

Even though the company calculates CAGR for customer growth, I think that this is a metric that can be analyzed sequentially (Q/Q):

Total customers grew 10.7% sequentially

Enterprise and Commercial customers grew 8.8% sequentially

Both of these growth rates are strong, specially considering that the company was near 1 million customers at quarter-end.

Just for a bit of context, DocuSign considers enterprise customers as companies generally included in the Global 2000 and commercial customers as mid-market and SMBs outside of the Global 2000. DocuSign also provides a metric that shows how many big customers the company has. This metric is customers with more than $300,000 in Average Contract Value:

Source: DocuSign’s Quarterly Earnings Presentation

As you can see, the company is also growing their big customer accounts, with an increase of 74 customers with more than $300,000 ACV in the quarter, an increase of 12.4% sequentially. It’s important to note that this metric does not necessarily imply that these customers are new because any given existing customer that grew its contract value over $300K for the year during this quarter would automatically be included in this group.

As we will see later on, the company made a special announcement regarding the number of customers during the earnings call.

Billings

This is another important metric to evaluate the performance of the company. The company includes in billings amounts invoiced to a customer in any given period. While revenue is recognized over the contractual period, most of DocuSign’s customers pay in annual installments one year in advance which means that the company is generating cash that it still can’t recognize in revenue. For this reason, billings is a leading indicator of revenue.

Source: DocuSign’s Quarterly Earnings Presentation

According to management, billings benefited from strong customer demand which brought early renewals and expansions. Renewals and expansions are directly reflected in Billings so this metric outperformed management’s expectation for the quarter. Second consecutive quarter over $500 million in billings.

Net Dollar Retention

This metric measures the ability of the company to upsell their products to existing customers. If above 100%, this means that the company is being able to increase the Average Contract Value of existing customers which is a positive sign of product stickiness and the company’s ability to upsell their products.

Net Dollar Retention has been improving steadily during the last quarters:

Source: DocuSign’s Quarterly Earnings Presentation

The same way as with costumers, it makes sense to analyze this metric sequentially rather than on a Y/Y basis. Net dollar retention for the most recent quarter stood at 125% which means that the customers that were already existent during Q1 2021 have a 25% higher AVC (Average Contract Value) in Q1 2022. This is a record for DocuSign as a public company.

Gross Margins

DocuSign discloses both Non-GAAP (adjusted) and GAAP Gross Margins. The difference between both is that the adjusted measure does not include stock-based compensation, amortization of intangibles or employee payroll tax on stock transactions.

GAAP Gross Margin was 78% for the quarter. This is a 300 basis points improvement with respect to the comparable period (Q1 2021).

Non-GAAP (adjusted) Gross Margin stood at 81% for the quarter and also showed an improvement of 200 basis points with respect the comparable period (Q1 2021).

Subscription Gross Margin (non-GAAP) was 85% for the quarter, higher than overall gross margin as you would expect. This number was up from 84% in the comparable period.

As you can obviously see, these are very high gross margins, proper of a high quality SaaS company.

Profitability

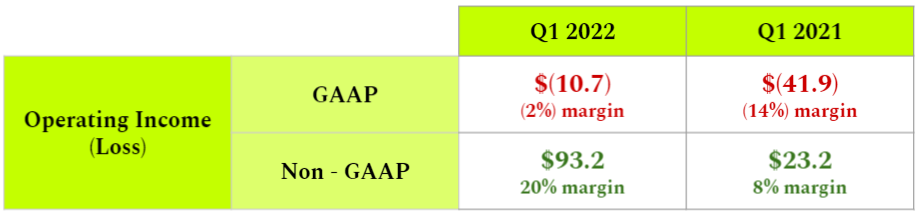

The company calculates both adjusted measures (Non-GAAP) and GAAP measures of operating income. Adjusted measures don’t account for expenses that are not tied directly to the company’s performance such as stock-based compensation expenses and are commonly used by growth companies to better measure the operating performance of the core business. In the following table you can see a summary of operating income (loss) for the current quarter (in millions):

Source: Q1 2022 Earnings Presentation

Although the business is still not profitable on a GAAP basis, profitability is improving fast and the company could breakeven soon if this trend continues. On an adjusted basis the company achieved their best margin up to date for any given quarter. This was mainly caused by top line outperformance that caught management by surprise and didn’t allow them to invest into this growth:

Yes, the operating margin was pretty phenomenal at 20%. In some ways we would have liked to be able to invest more quickly into that growth and bring down that number. It’s just very difficult to do in quarter. So, we’re really looking through the year at ways to continue to invest for growth.

To be honest, I was delighted to hear the above in the Earnings Call because it means that management is clearly focused on investing for future growth even if they have to sacrifice current operating margins. Exactly what you would like to hear as a growth investor.

Taking a look at the bottom line, the company also reports both a GAAP metric and a non-GAAP metric.

The company reported GAAP net loss of $(8.35) million which significantly improved when compared to previous comparable period. GAAP net loss for Q12021 was $(47.8) million

On an adjusted basis (non-GAAP), the company reported income of $91.8 million, an increase of 281% Y/Y.

If the company continues to outperform we should expect to see GAAP profitability soon. Recall that for the past three full years, DocuSign has reported GAAP net income losses.

Cash Flows

This is one of my favorite indicators because it actually shows how much cash the company is generating. “Accounting” profitability is obviously good and should be achieved in the long run but, in my opinion, the business model of any company should be first assessed from a cash generation standpoint (assuming that this cash is not coming entirely from debt or stock offerings of course).

Cash Flow from Operations (CFO) was $135.6 million in Q1, an increase of 129% Y/Y. The CFO margin for the quarter was 28.9% compared to 20% in Q1 2021. This improvement was driven by increased contract expansions and renewals which directly affect cash flow. Recall that DocuSign collects annual payments one year in advance so this metric is quite volatile if looked at on a quarterly basis and follows no particular pattern:

Source: DocuSign’s Quarterly Reports

Free Cash Flow was $123 million, an increase of 275% Y/Y. FCF margin for the quarter was 26.2%. Free Cash Flow margin for the same period of the prior year was 11%. As Free Cash Flow is calculated as CFO minus CAPEX it was affected by the same elements as CFO.

Earnings Summary

Overall, the company performed brilliantly, the growth story remains intact and DocuSign has a long runway ahead. Management continues to execute flawlessly and is very focused on making significant investments towards future growth which is something that you would like to see in a company that just grew their top line 58% Y/Y. Here you have a summary of the metrics that were discussed above:

Source: DocuSign’s Earnings Presentation

Guidance

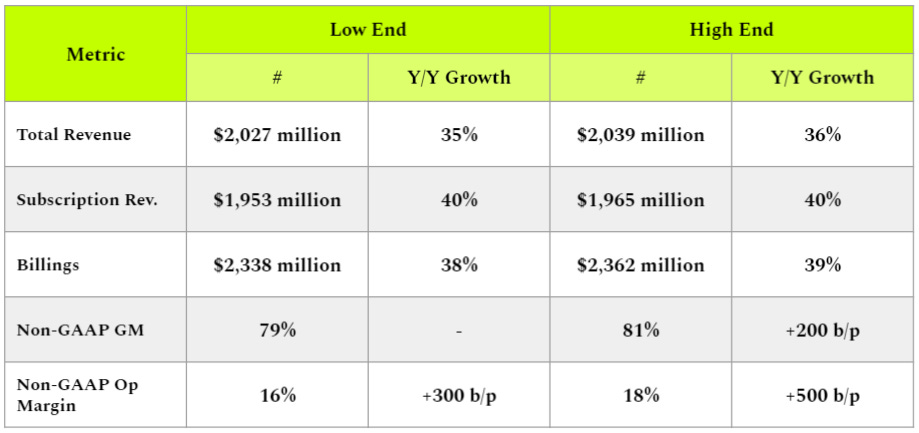

The company provided guidance for next quarter and for the full fiscal year 2022.

Quarterly Guidance:

Source: DocuSign’s Earnings Presentation

Strong continued growth into next quarter with billings expected to remain above $500 million for the third consecutive quarter. Sequential decrease in operating income margin due to increased investments in growth.

Full Fiscal Year 2022 Guidance:

Source: DocuSign’s Earnings Presentation

Remember that DocuSign has beat revenue estimates 100% of the time!

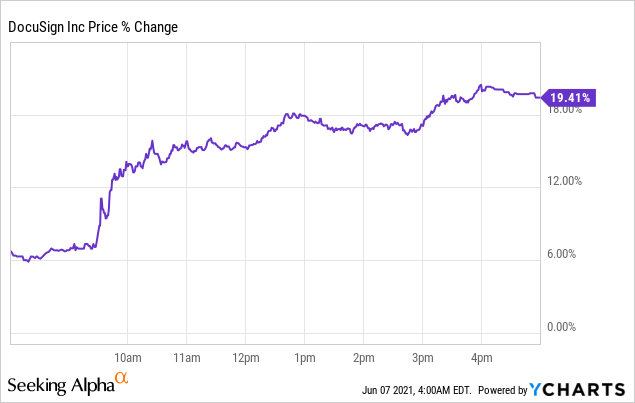

Reactions post-earnings

After a blowout quarter, the stock was up 19.8% during the next trading day.

Source: Seeking Alpha

Why did the stock skyrocket in just one day? The market is completely unpredictable in the short term and I am probably the worst investor out there timing short term movements but there might be some potential reasons for this strong movement.

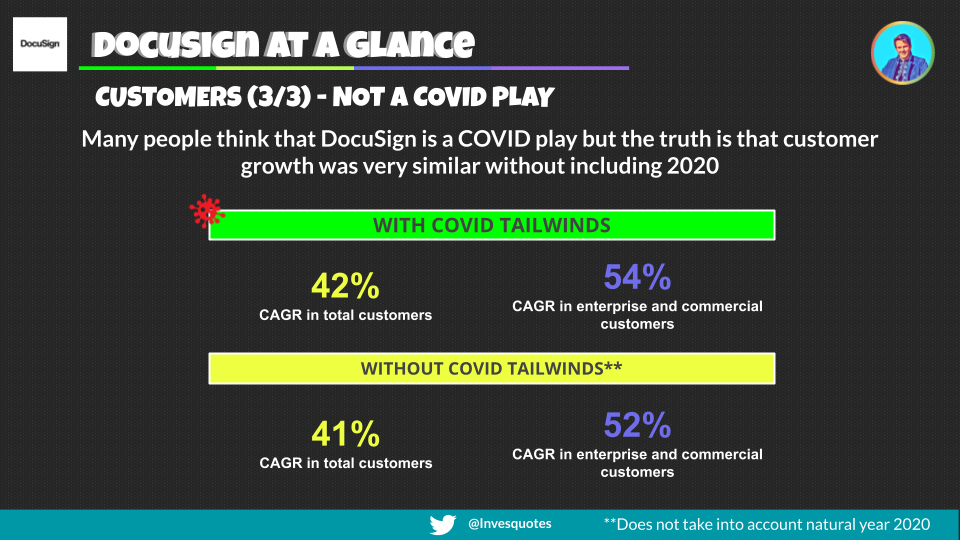

1/ Investors thought of DocuSign as a COVID play and they expected that with a reopening economy the company would not be able to sustain the high growth.

If you have gone in depth into the company, this argument should make no sense for two main reasons:

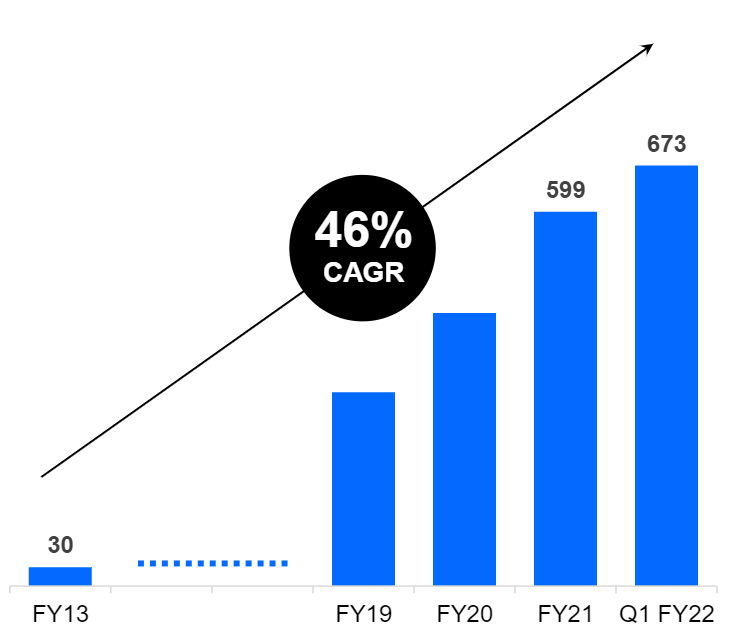

On the quantitative side, the company was growing at similar rates before the pandemic. This is a slide that I built a couple of months ago to show that this was not a WFH (Work From Home) company:

On the qualitative side, COVID obviously provided customer acquisition tailwinds but, in my opinion, this effect is unlikely to be reversed with the vaccine rollout because once the company’s customers have entered into an automated process it’s unlikely that they will go back to paper based agreements.

2/ The company announced the 1 million customer mark

During the earnings call, CEO Dan Springer announced that a few weeks ago the company welcomed their one millionth customer. The company also announced this achievement in their Twitter account:

This means that the company has added about 12,000 customers in a bit more than one month!

3/ The stock has not moved in almost a year

Even though the company has outperformed in every quarter, the stock has not moved in almost a year. This might be due to several reasons like a rich valuation or share dilution but in my opinion this has provided a great opportunity to keep adding if you are long.

Source: Seeking Alpha

What now?

DocuSign has the following characteristics which made me go Long:

It’s a high growth quality company

Indisputable leader in their market

Business showed resilience during the pandemic

Still in early days of a huge opportunity ahead

Top-tier and visionary management

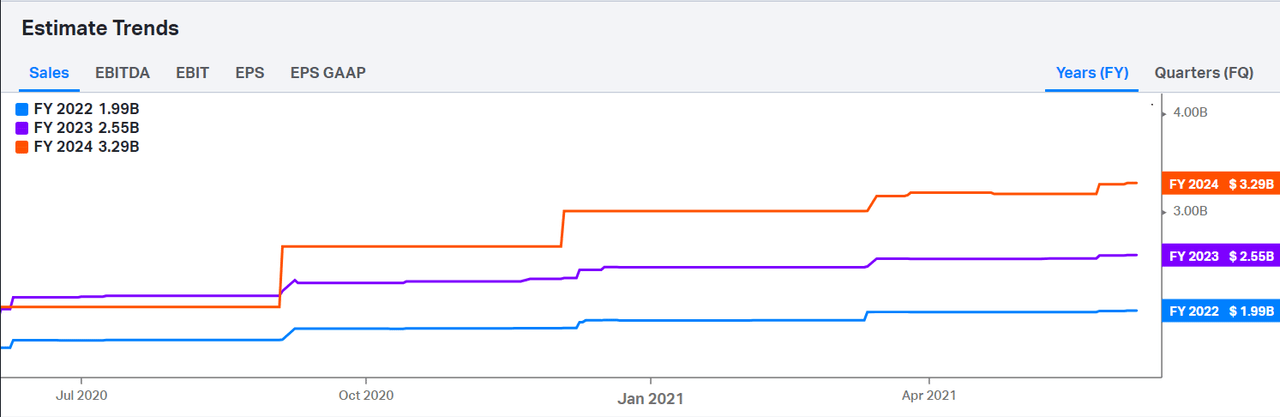

These characteristics are making it difficult for analysts to take a hold of this company. Take a look at the following graph:

Source: Koyfin Charts

This graph tells you what the estimates for FY 2022, 2023 and 2024 were at any given point in time. As you can see, the outperformance of the company quarter after quarter has led analysts to upgrade their estimates, they just don’t seem to get a hold of what this company is capable of until they are proven wrong. The fact that, in July 2020, FY2023 sales estimates were above those of FY2024 estimates may be due to faulty data.

I plan to hold my shares for the foreseeable future as long as management continues to execute and the growth story is intact.

Stay well!

IQ

Disclosure: I’m long $DOCU