If you are a current subscriber, welcome back to another article. If you are a new reader and want to have access to future articles and deep dives of “The Global Investor Newsletter”, make sure you subscribe!

While our new Deep Dive on FarFetch is still on the making, we thought about writing about a topic that we both like to think about. On this brief piece we’ll discuss how it’s ok to be wrong and how to avoid focusing on the wrong things when investing.

Hope you all enjoy!

Most investors share a common fear: being wrong. Although in this context you can already imagine that we will be talking about the stock market, this fear is extensible to almost any aspect of life.

Have in mind that there are only three sure things in life:

Taxes

Death

Being wrong (eventually)

Being wrong always hurts but it hurts even more when your money is at stake.

This said, in investing, being wrong is not only acceptable, it’s in fact part of the game. One could argue that it is something even necessary to generate long term returns. If you can’t cope with being wrong then individual stock investing is not your game, you should give index ETFs a try.

Let’s start by laying out some practical examples by non-average investors.

The greatest investors make mistakes

Even the greatest investors, those who have beaten the market consistently over long periods, have consistently made mistakes throughout their careers. Let’s guide you through a couple of examples.

Warren Buffett

The Oracle of Omaha has made many mistakes throughout his investing career and he has always been open to share them with Berkshire’s investors.

We will look at one of his first mistakes and one of his last mistakes to evidence that even the most experienced investors keep making mistakes regardless of their experience.

Do you know what was his first mistake? Buying Berkshire Hathaway.

My first mistake, of course, was in buying control of Berkshire. Though I knew its business -textile manufacturing – to be unpromising, I was enticed to buy because the price looked cheap. Stock purchases of that kind had proved reasonably rewarding in my early years, though by the time Berkshire came along in 1965 I was becoming aware that the strategy was not ideal.

This may be one of the reasons why Warren Buffett evolved from cigar butts to buying higher quality companies even if the price was not so cheap. Charlie Munger also played an important role in Buffett’s transition to high quality.

Intelligent and savvy investors learn from mistakes and adapt. Buffett made a lot of money with Cigar Butts but he knew that this strategy was not the best for a buy and hold investor which is why he decided to change his approach. Buying high quality companies with large moats has allowed him to be “less worried” about his portfolio.

Although at the date of this mistake Buffett was already an experienced investor, it was still very early into his investing career. This may lead some to think that as his investment career has progressed his mistakes have been drastically reduced. This is far from true.

Let’s fast forward to the most recent Berkshire Annual Letter for Shareholders (2020). In this letter, the Oracle of Omaha points out another mistake he made which cost Berkshire’s shareholders $11 billion. As it is true in almost any investment, successes and mistakes take time to show up, this one took 4 years:

The final component in our GAAP figure – that ugly $11 billion write-down – is almost entirely the quantification of a mistake I made in 2016. That year, Berkshire purchased Precision Castparts (“PCC”), and I paid too much for the company. No one misled me in any way – I was simply too optimistic about PCC’s normalized profit potential. Last year, my miscalculation was laid bare by adverse developments throughout the aerospace industry, PCC’s most important source of customers.

I believe I was right in concluding that PCC would, over time, earn good returns on the net tangible assets deployed in its operations. I was wrong, however, in judging the average amount of future earnings and, consequently, wrong in my calculation of the proper price to pay for the business.

PCC is far from my first error of that sort. But it’s a big one.

Source: Berkshire Annual Shareholder Letter (2020)

Despite Buffett and Munger making numerous mistakes, this is how Berkshire has fared since 1990:

A 35% CAGR approximately, not too shabby.

Since inception (1965), Berkshire has achieved a 20% CAGR, almost doubling that of the S&P500 (10.2%).

As you can imagine, these mistakes are two among many mistakes that Berkshire has made, but it didn’t stop the company from significantly beating the indexes. As we will show throughout the article, this is possible due to a combination of several factors.

Let’s see the example of another one of the GOATs.

Peter Lynch

Lynch’s fame is warranted as he was able to achieve a 29.2% CAGR for 13 years working as a manager of the Magellan Fund. For a little bit of context, a $1,000 initial investment with Peter Lynch during these years would’ve turned into a 13-year ending balance of $27,950.

And yes, you guessed correctly, despite having such an impressive track record, he made many mistakes during his career.

Although not conventionally seen as a mistake by those investors who only fear losses, Lynch’s biggest mistake was selling too soon. He openly describes this mistake and talks about Toys R Us and Home Depot as his two biggest mistakes:

It’s pretty clear that mistakes can come in many shapes and forms. Some might consider a mistake buying companies that go to 0 or significantly decrease in value and others might consider a mistake selling companies that later 10X. Both are mistakes and the latter is much more worrying than the former because you will definitely lose much more money.

When you sell a winner too soon you are potentially losing an unknown amount of money that could technically go to infinity. This basically means that gains are uncapped. On the other hand, when you hold a loser for too long, even though this is a mistake, it will only cost you a maximum of 100% because downside is capped. All of this assumes of course that you are a long investor because if you are a short investor, the story is exactly the opposite. We like to call it Asymmetric Win-Loss Rate.

Mistakes can’t be avoided but they can indeed be minimized. These are some things that you should take into account when you invest so that you can hopefully minimize your mistakes over the long run.

Love does not pair well with investing and should be left to your personal life

If we search for “Love definition” in Google, we get the following:

An intense feeling of deep affection.

Any investor should see at first sight what’s wrong with loving any particular investment. Yes, it’s the word “feeling”.

Many of us would agree that the hardest part of investing is detaching of emotions when making decisions so “loving a company” should be something that you should try to avoid. You can certainly be very optimistic about any particular company but don’t fall blindly in love with it because it may lead you to making fatal mistakes.

Let’s see a real life example. Go back to when you had a girlfriend/boyfriend and you were so in love that you didn’t see that he/she was no good for you. While you were dreaming and everything seemed perfect, your friends could clearly see, as if it was something obvious, that the relationship was no good for you and it was toxic. What can we learn from this experience? Blind love blocks rational thinking which is something that you should try to avoid at all costs in investing.

To mitigate this, if you feel you are “falling in love” with a company, try to talk to well informed bears so that they can lay out their detailed bear thesis. Many times you will see that many investors don’t even know the risks of their holdings as if their companies were just perfect. Spoiler alert: if you are getting a return, there is risk. Find out what risks are inherent to your investment and weigh them against potential returns.

Cutting losers and not losing sleep over winners you don’t own

Admitting that you were wrong when fundamentals are weakening and your position is down 40% is hard because hope is the last thing humans lose. How many times have you heard the following?

I’ll wait until it breaks even and then I will sell it. - Every investor at least once during his career

This is commonly know as being high in hopium. The truth is that, when hope is not backed by some kind of fundamental value, it becomes an illusion and a dream.

Hopium is based on the false belief that, if investors are patient, stocks will eventually break even. We could write a whole article with examples of stocks that never came back to previous highs but we don’t think that readers would enjoy a +500 page article. I (Invesquotes) am guilty of falling in hopium with the stock of Banco Santander. I bought the stock because it was “too low when compared to its highs” only to sell it at a 30% loss when I realized that this was not a valid investment thesis:

Some stocks come back and break new highs while others don’t, what is the difference between them? The evolution of the business. Here we have two possible cases when we are holding an unrealized loss:

If the business continues to outperform in every metric but the stock price action is ugly, you can hold fairly confident to your loss and consider yourself a bagholder. I am currently bagholding Teladoc and Pinterest because the businesses are performing as I expected when I bought.

If on the other hand, the business is showing weakness in its core fundamental metrics for a prolonged period then you will probably be better off selling your position, even if it is at a big loss. Will this hurt? Yes. Is it something that will benefit your returns over the long term? Yes.

Don’t hesitate to realize losses when necessary. Selling a stock at a loss because you don’t fully understand the business is also fine. The objective of any investor should be to have a portfolio which he is comfortable with.

The same applies to “The One That Got Away” syndrome some time on our investing path, something we all have suffered of. The phenomenon consists of selling a stock too early, only to see it rocket right after.

The common investor usually suffers immensely from this event, almost like he or she had lost money from it. Well, as logics points, he/she didn’t. Nevertheless, this is another situation where emotions take over, and the feeling of being over fills the investor over something that should have instead taught him a lesson.

Buy&Hold suffered from this like many others. After doing all the DD on POSI3, a Brazilian company, he sold after a 30% gain, only to see this happen right after:

Rather than focusing on the 30% gain and right thesis, I felt the same pain as I would in losing everything in a Call or a Put. Rookie Mistake.

Takeaway: Cut losers and don’t lose your mind over what you don’t own.

Normalize changing your mind

Two rules are eternal in investing:

You won’t get extra points for difficulty

You won’t get better returns if you don’t have an open mind.

Investors overall tend to get affected by their stocks in an emotional way. That emotion leads to pride, and that pride blinds you from the beauty that is changing your mind. Pride has a similar effect than falling blindly in love.

The ability to admit you got it wrong and selling or admiting that it’s not too late and buying in is a great trait for any investor. Being open minded and lowering your ego barriers changes the landscape, not only on the investment front, but on the personal front.

We assure you that every single one of the greatest investors got it all wrong at least one time, and they all admitted their mistakes fast and directly. In fact, we already showed a couple of examples involving two of the greatest investors of all time.

So if you know you’re gonna be wrong eventually, why are you so obsessed on always being right? Are you really caring take care of your money? Or are you taking care of your ego? We personally prefer to make most of our mistakes early in our investing careers rather than when our portfolio is much larger and we have more responsibilities.

The most important principle of finance:

A dollar today is worth more than a dollar tomorrow.

Can also be applied to mistakes:

A mistake today is worth more than a mistake tomorrow

Mistakes compound the same way money does.

The intelligent investor has to pay attention to these traps set by themselves. Emotions and investing are inevitably linked and there is nothing wrong with this but your biggest enemies are those emotions you lose control of.

Don’t try to avoid emotions because this is not possible. Focus on controlling them.

Sometimes you earn and others you learn

By now it should be pretty clear that investing mistakes are unavoidable so what can we get from them? We personally view investing as a win-win game considering that we are still in the very early innings of our investing careers. Let’s see why.

There are two possible outcomes when we make an investment: we can be right or we can be wrong. Both have positive sides to it.

When we are right, we make money (earn).

When we are wrong, we are reducing our future mistakes (learn).

You have to take into account that you can be wrong and make money too. This can happen when you lay out your bull thesis and the stock goes up for reasons that are not included in it.

For us, it’s that simple. The advantage for any long investor is that when you are right and you earn, you will probably earn big. On the other hand, when you are wrong, your maximum loss is 100%, considering that you take all this time to realize that the business is not performing accordingly.

This is the asymmetric win-loss rate that we talked about before and it’s one of the greatest advantage for long term oriented investors. Its power is sometimes under appreciated but creating a numerical example can help you uncover its potential.

You don’t have to be right all the time to be a successful investor - A practical example

All it takes is a couple of big winners to make up for the rest of the losers.

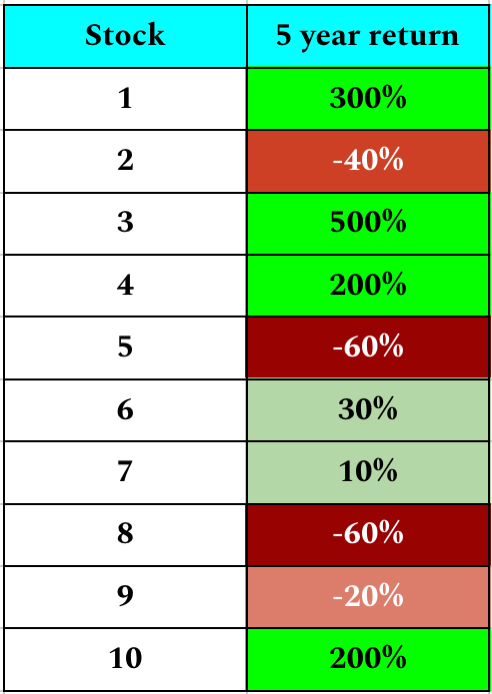

Maybe this is not so easy to understand, especially for newer investors, so we prepared a practical example. Let’s imagine that you build an equally weighted portfolio made up of 10 companies and over the next 5 years, these stocks perform as follows:

Assuming that we you initially invested $100 dollars in each of these companies, your starting balance would’ve been $1,000. At the end of the 5 years, your ending balance would be $2,060 (400+60+600+300+40+130+110+40+80+300=2,060) which would provide a CAGR of 15.6%, beating that of the S&P500.

This quick example shows that, even if you get wrong 40% of your investments, you can still manage to beat the market by holding onto your winners. In fact, the gains from stocks 1 and 3 were already enough to make you earn some money even if the rest all went to 0 (of course, this return would not beat the market but would help you preserve your capital at least).

This example assumes that the investor pours in the money at the beginning and doesn’t touch anything until the end. If we included the ability of the investor to reallocate capital across the portfolio then results would be very different depending on the investor’s actions:

A good investor could significantly improve the returns of this portfolio by cutting losers and adding this proceeds to his/her winners.

A bad investor could worsen the returns of this portfolio by letting losers drop thinking that they could come back while selling winners too soon thinking that they were too high.

If you want an example, IQ put this thread together a long time ago. The study obviously suffers from survivorship bias but it also assumes that the investor was only right 10% of the time which is pretty low:

Although mistakes are inevitable, it’s pretty clear that the key to achieve worthwhile returns is to reduce errors as much as possible. In our opinion, there are some key traits that differentiate top tier investors from mediocre investors.

What differentiates great investors from mediocre investors?

Great investors are able to spot winners and losers sooner than mediocre investors. Their ability to detach from emotions helps them in this task

Great investors do extensive research. This way they are able to minimize their losers although they always acknowledge that they will inevitably hold them at some point. They avoid buying what they don’t know.

Great investors don’t borrow anyone’s conviction. This way they are able to ride through rough times and avoid selling winners too soon.

Great investors see the big picture. They don’t think about what their portfolio will look like in 1 year, they think about what it will look like in +10 years.

Great investors are able to block the noise. The market is a noise machine over the short term but will provide great opportunities for those that are able to separate signals from this noise.

Achieving what great investors achieve is very difficult but having these things in mind can help you get better and better everyday. Learning compounds.

Conclusion

With this short article, we tried to help you understand that not only you should not fear being wrong, you should welcome it. Every great investor has to go through periods of mistakes and it’s throughout these periods when great investors differentiate from mediocre investors.

We think that this quote by Epictetus sums it up pretty well:

It's not what happens to you, but how you react to it that matters.

If you leverage on all of the lessons you can learn from your mistakes, you will be one step closer to being a great investor. It takes time, but it can definitely be done. Don’t rush it, focus on rational actions and close out impulsive emotions.

Mistakes happen all the time, it’s OK to be wrong.

Stay well!

IQ and B&H

Great article and very good reminder :) Thank you very much !

Really enjoyed this. Thank you!