JD Q32021 Earnings Digest

JD Q32021 Earnings Digest

Coming for the Throne

Hello Global Investors,

Today we’ll be taking a look at a position most of you know I’m very bullish on, JD. My bullishness on China has been tested this year by macro and regulatory factors. However, JD once again shows me that the focus should always be on the business, price is only a detail. In today’s article, I’ll dissect those earnings and tell you what key takeaways I got from it.

This piece will be free for all subscribers to access, but most will not be. That said, If you want to have full access to this article and all future and present content from The Global Investor content, consider subscribing for the paid version and testing it out.

A quick Disclaimer before we start: I am not an analyst of any asset and this piece is not investment advice of any kind. The article’s goal is to be instructive in educational purposes and must never be interpreted as a call for a buy or sell of any stock. Do your own Due Diligence.

Now let’s go

JD reported its Q32021 earnings and - on the same day that Alibaba disappointed the market - proved its growth runaway is far from over. Posing strong numbers on all fronts, JD is now one of the leading forces for non Chinese investors returns, and it might be only the beginning. All that said, let’s start slow, with the numbers

Financials and Numbers

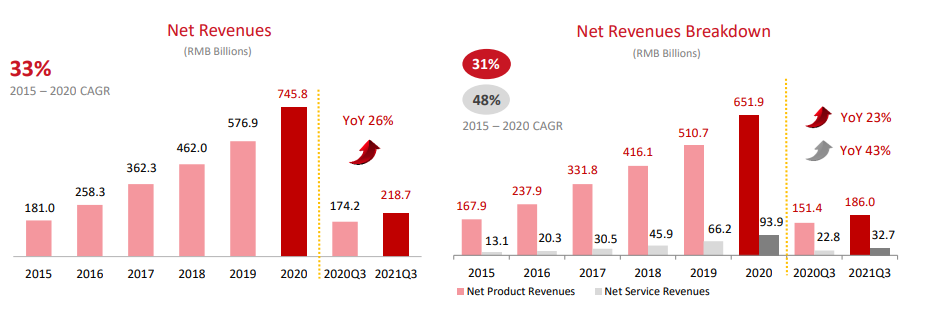

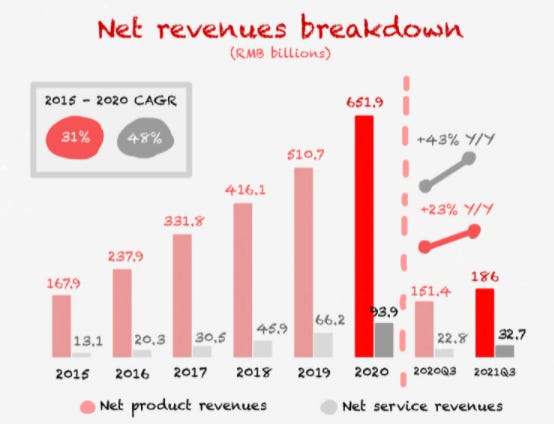

Revenues and EPS

Starting with the headliners of all earnings, revenues grew by 25.5% compared to Q32020 super tough comps, reaching RMB218.7 billion (US$33.9 billion). That number is even more impressive when we look at the sustainability of CAGR from JD throughout the years. For the last 3 Q3s - meaning 2018, 2019 and 2020 - JD has achieved a revenue CAGR of 27.5%. Although the revenue has gotten bigger, growth hasn’t slowed down and this quarter once again defies the law of large numbers and shows JD’s large runway for growth.

JD separates revenues in Product Revenues and Service Revenues. First, on Product Revenue, we have General Merchandise Revenue and Electronics and Home Appliance Revenues, so essentially what JD gets by selling on their marketplace from their own inventory (i.e JD selling without merchants) the so called 1P marketplace. The reason why JD separates Product Revenue in these two sections is due to the margins on General Merchandise being higher than Electronics and Home Appliance, so we can better evaluate the way margins will develop.

Product Revenue is by far the bigger slice of the pie and it grew by 23% Y/oY, to about US$ 28 billion. The already good number gets even better when noted that General Merchandise keeps growing more than Electronics and Home Appliances, 31% and 22% respectively. According to management, the reason behind this continued growth is mainly due to the supermarket section on JD’s marketplace:

“General merchandise revenues grew 29% year-on-year and 32% 2-year CAGR in Q3. This was mainly driven by the 35% 2-year CAGR of our supermarket 1P order volume growth in the quarter. I want to share a few observations of our supermarket categories. First, supermarket categories were again the largest contributor of our new users in this quarter. Second, the average number of orders per user for supermarket categories continued to increase and reached its all-time highest level. Third, users are purchasing more highfrequency supermarket products on JD, including food and beverage, fresh produce and baby and maternity products. All these have helped drive our daily user engagement meaningfully” - Xu Lei, JD’s President

This is an important core for JD to develop, supermarkets don't have the best margins in the world but it’s a great way to acquire customers to the platform - and cross sell - especially those from lower cohorts, where the initial ticket is lower.

On Service Revenue JD includes Logistics and Other Services and Marketplace and Advertising Services. This is where JD charges its take rate for the goods sold in their marketplace and for services delivered to merchants like ads and better placement in the app and other services from JD Health and JD Log. Obviously this is a mix bag with mixed margins but it’s important to see it grow so JD keeps building a stronger ecosystem. Logistics and Other services grew at 53% rate, passing Marketplace and Ads revenue, which grew 35%. However, this is still the smaller part of the business (thus growing faster), representing only 15% of the total revenue.

JD doesn’t provide guidance, but paying attention to the call you can pretty much scoop it out that management is excited for the future:

“Okay. Let me add on the outlook for Q4. So there are few factors I would like to highlight for JD Retail. One is that the user growth is still is -- the growth driver for JD Retail, we expect JD Retail continue to deliver quality growth in terms of total user base, user engagement and stickiness as they continue to reinforce the consumers mind share. Second, the supply chain disruptions for certain products remain unchanged and existing as we just discussed. So this will affect the growth of our 1P business to a certain extent, in particular, the mobile phones and electronics categories. However, as Xu, Lei mentioned, based on the strengths of our supply chain capacity, we expect that we can create even more value and certainties for our business partners in this changing environment and continue to outpace the industry growth for these categories. And then third, with the implementation of 3P ecosystem and omnichannel strategy, since the beginning of this year, the 3P business is growing well on our platform. And so the 3P merchants served as a great supplement of our 1P business for the categories that are facing supply chain disruptions. So overall, we expect that the growth of 3P will be faster than 1P in Q4, similar to what you have seen in Q3” - Xu Lei - President of JD

On EPS, we had a bright spot in the ER. JD beat the consensus by almost 50%, reaching US$ 0.49. As we are going to see forward. I wouldn’t make such a big case of this data since JD margins structure is still super volatile and far from having an established runaway. You can get what I’m saying when we look at the Operational Income, where JD reached US$ 400 million, a 45% decrease Y/oY. Inconsistent yet, but well inside plan as we’ll see.

Margins

JD margin structure is still one of the main focuses when talking about a bear case. The company has reinvested most of its profits, thus creating razor thin margins that sometimes even will lead to losses. I stated my opinion on JD’s Deep Dive for this newsletter (click here to give it a read) and I stand by it. As stated by management (several times) the focus now is on growth and margin expansion will come later.

Taking a deeper dive on margins, the one that deserves the main focus is the gross margin. That’s because gross margins show the potential to be unlocked on a company’s financials, especially on growth companies in which we don’t know their full potential. Gross margins for JD are where they have been for the last 4 years, at 14%. This number has been a consistent one in margins since forever and although is fairly low for a tech giant (but normal for a retailer), it’s openly not a worry for management right now.

Of course that - as with any other stocks - margins are a risk for JD, if management doesn’t comply with its promise the case would have a fairly lower upside. However, JD has executed almost to perfection, so I don’t see a reason to not give them the benefit of the doubt

“So looking ahead, I would say our expectation on the margin profile or margin trajectory remain unchanged. In the short term, we may be facing the drag from the category mix shift as well as the change of the business model. But as JD has been continuously building our capabilities in the supply chain through -- and improve the operating efficiency of inventory management through technology, so we can gradually improve the margin, I would say, in the long term steadily” - Xu Lei, JD”s President

As you see above, JD’s is laser focused on growth ala Amazon in the 2000s, they maintain this line of thought since 2016 earnings calls. As per the JD Deep Dive, I believe this margin has a lot of room for expansion so I’m happy with it.

Expenses

Cost of Revenue

On the expenses section, JD had accelerated growth in some fronts worthy of attention. The first one is Cost of Revenue. Cost of Revenue are all the costs involved directly on the creation of the streams of Revenue (i.e cost of producing goods). JD’s Cost of Revenue grew by 27.3% to RMB187.6 billion (US$29.1 billion). The last 3 years Q3 Cost of Revenue CAGR is of about 27.6%.

As you can already guess where I’m going with this, you can see that both the CAGR and this quarter Cost of Revenue growth are higher than the revenue growth. This, of course, is not good, since it means.

Operational Expenses

Now, let’s focus on Operational Expenses for a bit. OpEx is important for us to better understand where JD is investing and how effectively it is generating ROIC. For this section, Since it’s an asset heavy expense, I’ll exclude Fulfillment from Operational Expenses. This way we can better focus on Sales & Marketing and General & Administrative, where I have some points to make. Also, I’ll not about Research and Development, since it stayed flat and without any comments by management.

Marketing

Marketing Expenses doesn’t need much explanation but it’s one of the most important metrics for e-commerce businesses. In these businesses marketing expenses are always high but stop growing and stabilize when the company reaches maturity. For Q321 Marketing Expenses surged 42.3% to RMB7.8 billion (US$1.2 billion) Y/oY.

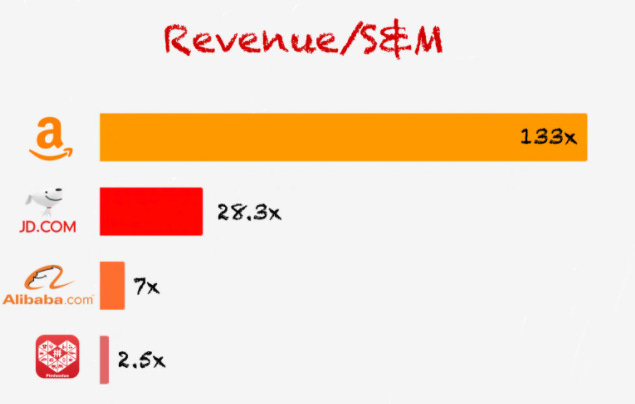

The marketing growth being much higher than the revenue’s one is not good. However, before we jump to any conclusions, it’s worth taking a look at one of my favorite multiples - as a lot of you already know - Revenue/S&M. This metric shows how much a dollar spent on marketing generates in revenue, meaning the efficiency of the OpEx (or ROIC like I said above).

JD’s Revenue Revenue S&M currently sits at 28.3x. As a comparison JD’s main competitors Alibaba and Pinduoduo have a 7x and 2.5x multiple respectively. So, when looking at competition it’s clear that JD has an advantage on that front. Of course it can - and should - get better, some international players show how ROIC on the S&M can reach almost perfection, Amazon being the best of them, currently sitting at a 133x Revenue/S&M.

Point being, revenue growing less than Marketing is a common strategy to leverage sales, especially during holiday’s season, like Single’s Day in China, which had campaigns starting months ago. That said, shareholders should always pay attention to the S&M curve of growth, being that the goal here is the multiple to expand and not contract by a slow down of revenues and an increasingly higher Marketing Expense.

General and Administrative

General and Administrative expenses increased by 91.1% to RMB3.1 billion (US$0.5 billion). The reason why I’m tackling this expense is due to the reason behind this huge growth, SBC Expense. The Stock Based Compensation increased by almost 600% Y/oY, this absurd growth has begun in the last quarter and came through to this one.

Now, although this is in my opinion the worst part of this report, I have to say that almost all growth companies have quarters with a surge in SBC Expense. The real problem is not a periodical increase on SBC but a constant one. Twitter for example has a constant surge in SBC for years and that has become a real problem for it.

I’ll give the benefit of the doubt to JD, but this has to be watched super closely for the next quarters and, if it continues, I’ll dig deeper on it and consider a red flag depending on what I find, I suggest any bulls or bears do the same.

Other Numbers

Before we move into the business section, here are some other numbers you should pay attention to:

Cash in hand was flat at US$ 13 billion as was Debt at US$ 450 million

Free Cash Flow decreased by 44%

Inventories were also flat, this is an issue in my opinion, supply chain issues are probably here to stay, so an anticipation in the turnover like Mercado Libre or Amazon would be good to see. That said the turnover did decrease from 4 days to 32 days, which is positive.

The Business

Now let’s take a look at some highlights from each one of the businesses.

E-commerce and Retail

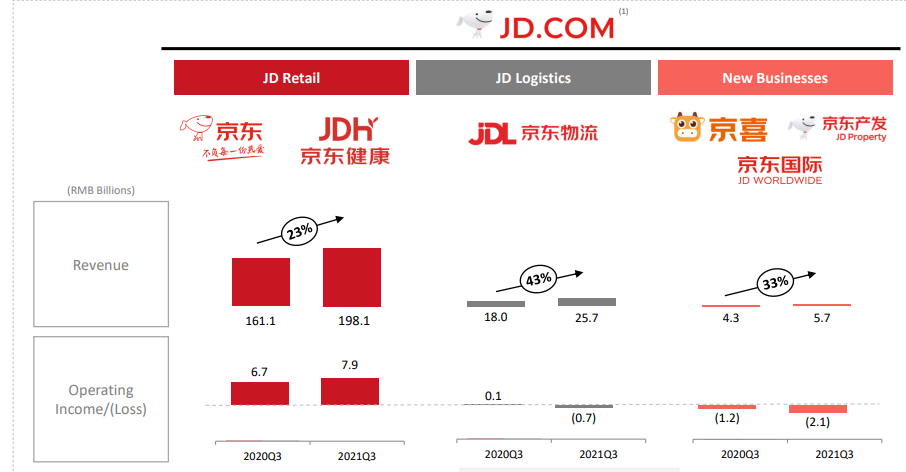

The main driver of JD keeps growing at an outstanding rate. With 23% growth the section that includes the e-commerce and O2O business, JD Health and Jingxi are showing resilience amidst an increasingly worst macro.

“With resilient business operations and core competencies in technology and supply chain, JD has built a unique business model, enabling us to have better control across the entire business process,” said Lei Xu, President of JD.com. “This powerful competitive advantage allows us to navigate through economic cycles and increases our ability to create value as a new type of real economy based enterprise. As a result, consumers and business partners increasingly trust and rely on JD, and we were able to outpace the industry growth in China in the third quarter.” - Sandy Xu, JD’s CFO

That resilience has to do with two main drivers, a moat with a self owned supply chain and high quality services and an ability to navigate a regulatory scrutiny ambience without suffering as much as its peers. So where does that resilience take us? Well It’s early to tell but there are signs that JD is taking market share from some of its main competitors, Alibaba and Pinduoduo.

After disappointing earnings from PDD and BABA (Alibaba growing at 14% organic growth and Pinduoduo missing revenues estimates by 50%), while JD impressed the market, it was clear that either macro is indeed slowing down but JD is taking market share, or macro is not slowing down but JD is the only one able to capitalize. I believe option number one is more probable. Now of course that is still too soon to reach any conclusions, so the overall scenery has to be watched closely for the next quarters.

The advantages from the moats I talked about here become even clearer when we look at the preference of sellers. According to JD, the number of sellers is up 3x Y/oY, and the NPS metrics are also up. According to management, that preference is leading to an increasingly faster growth on 3P than 1P. Let's take a look at what Sandt Xu, JD’s CFO, said about this:

“The supply chain disruptions for certain products remain unchanged and existing as we just discussed. So this will affect the growth of our 1P business to a certain extent, in particular, the mobile phones and electronics categories. However, as Xu, Lei mentioned, based on the strengths of our supply chain capacity, we expect that we can create even more value and certainties for our business partners in this changing environment and continue to outpace the industry growth for these categories. And then third, with the implementation of 3P ecosystem and omnichannel strategy, since the beginning of this year, the 3P business is growing well on our platform. And so the 3P merchants served as a great supplement of our 1P business for the categories that are facing supply chain disruptions. So overall, we expect that the growth of 3P will be faster than 1P in Q4, similar to what you have seen in Q3”

Lastly, on Jingxi, JD’s play on lower cohorts, we didn’t get much info. That’s a bummer to be honest. I was expecting a gradual release of data from Jingixi, but apparently they are not ready yet. The good news is that - as predicted in my JD Deep Dive - management stated the supply chain and ecosystem perks that JD has (being that it’s not a total standalone yet) is providing advantages when compared to other lower cohort initiatives, like Pinduoduo. Anyhow, Jingxi is still in early stages, although it has a lot of potential.

According to management, they are waiting to have Jingxi business model 100% validated before scaling it to the whole country. It is unknown how long this process might take, but I’d expect some news on it in the next couple of years.

“Since July, Jingxi has proactively shifted focus on 10 selected provinces where we are pleased to see improving supply chain efficiency and cost structure in Q3. In particular, fulfillment cost per order has lowered by nearly 50% compared to that in the early stage of the business, and user experience have largely improved as well. More importantly, thanks to our focused effort and investment in infrastructure, revenues generated by local group leaders and mom-andpop stores on Jingxi have been clearly climbing up. I hope that my sharing today has showed that JD is a new type of real economy-based enterprise that has the traits of both real economy and digital technology capabilities. Such type of enterprises will play an even greater role in China's economic development in a new era. From a long-term perspective, JD is strategically positioned to generate compelling growth opportunities despite the current complex and evolving macro environment.” - Xu Lei, JD’s CEO

Logistics

On the logistics side, JDLogistics had an awesome showing. JDLog grew revenues by 43% this quarter, while reaching 1.300 warehouses owned or operated. Now, margins - like on the rest of the company - are not there yet, JDLog had a really small operational loss, after a small profit in Q32020.

The company is walking towards full profitability but for the margin structure to stabilize, it will still need time and the road will for sure be bumpy. This road without a doubt goes through JD Logistics becoming a more independent company from the JD ecosystem. That will take time of course, since - besides being the leader - JDLog has 5% of the logistics market share in China. That said as we see down below, management is giving great signs:

“External revenues continued to account for over 50% of JDL's total revenue while reaching a historic high in this quarter”

I’ll make this section briefer than usual, since I really think JDLog is on the right path, but there will not be much flashy news on it worthy of a deeper analysis.

What to Expect

There are a few things I can’t even pretend to expect when we talk about China. From Government interventions to e-commerce slowdown there are a few things we cannot predict, so I’ll make my expectation on JD here based on a neutral (not too pessimistic or optimistic) premise.

I expect JD to deepen its moat and go for the throne in China. Debanking Alibaba is an almost impossible task, but I think JD is capable of taking enough market share for them to become an even more relevant player in Chinese commerce. That of course means margins will not get better anytime soon, and I'm ok with it as long as the growth sustains.

I expect Logistics to become a self-sustainable moat - meaning profitable - and Jingxi to be a CAC machine, meaning they’ll use the platform to create a considerable mind share between lower classes. Jingxi can be in my opinion a share taker from Pinduoduo, being leveraged by the logistics and high quality main commerce. Both of these things will take some time, but I’m not in any hurry.

With Xu Lei as President, I expect more innovation to come. The O2O and supermarket fronts are good starting points on his reign, but e-commerce - especially in China - is an industry where constant innovation is needed. He is the man I expected to take control in my Deep Dive, so I’m very much happy with that.

All in all, my expectations for JD are the best possible. I expect the current excellent execution to keep being delivered for the next few years. If this execution is actually delivered, my valuation as presented here will be as validated as it ever was.

Revenue growth as per management will probably be sustained for some time, but bad macro is always lurking. Although I see JD as one of the most resilient players when talking about supply chain issues, I think it is possible things will get worse next year and they are affected by it. Only time will tell but as you can see my bullishness remains after this ER.

Key Takeaways

This is a new section for my Earnings Digest where I’ll say my key takeaways from the quarter:

The Good Stuff

JD’s management is being coherent and honest with what has been said for the last couple of years, margins are being sacrificed right now due to not being the focus, growth is the focus and we can see that on the sustained high growth in all the essential sectors of the company

The e-commerce core seems like one of the most ready to face tough macro between all Chinese players. Expect JD’s moat to deepen.

Although it’s not 100% confirmed, there are once again strong signs JD is taking share from competition.

The Bad Stuff

Expenses are rising quickly, SBC and Cost of Revenue have to stabilize or the margin will never be sorted no matter the focus given to it.

Some focus points were not talked about enough, information lacked mainly on Jingxi

Conclusion

JD once again proved the doubters wrong. Execution has been close to perfect for a while now and the market has not appreciated that. Although JD rallied after the release, it’s still cheap, especially looking at how poorly competition has performed.

I remain bullish on it and will add on any drawdows.

See you soon.