Teladoc’s 2021Q2 Earnings Digest

Preparing for the future

If you are a current subscriber, welcome back to another article. If you are a new subscriber and want to have access to future articles, make sure you subscribe!

Summary

Teladoc presented 2021Q2 results in line with management’s guidance, posting a revenue increase of 109% Y/Y.

Organic revenue increased 41% Y/Y despite facing tough comps with the first wave of the pandemic (2020Q2).

Some investors didn’t like member growth (+1% Y/Y) and the fact that the company missed the street’s GAAP net income estimates.

The company is setting up nicely for the future as it advances on the integration of Livongo, launching MyStrength complete, the first integrated product.

The breadth of its offering is enabling Teladoc to sign important deals which will come into play in the beginning of 2022.

As most of you might already know, on the 27th of July, Teladoc (TDOC) presented its 2021 Q2 results and, even though the market didn’t seem to like these results, they were actually pretty strong if you understand Teladoc’s business and growth opportunity.

The objective of this article is to go through the results and demonstrate that the business is executing as expected, regardless of the short-term stock price action. Here I would like to give a tip. When a company reports earnings, you get much more value if you read the report thoroughly first and then look at the price action after that. If you do it the other way around, the way most people do it, you will probably read the report biased positively (in case the stock price is up) or negatively (if the stock is down).

I will divide the article into two main sections, the numbers and the background. I will quickly skim through the numbers, providing some commentary so they can be fully understood, and I will then focus a bit more on the qualitative side, which is much more insightful for long-term oriented Teladoc investors.

Without further ado, let’s get started!

The Numbers

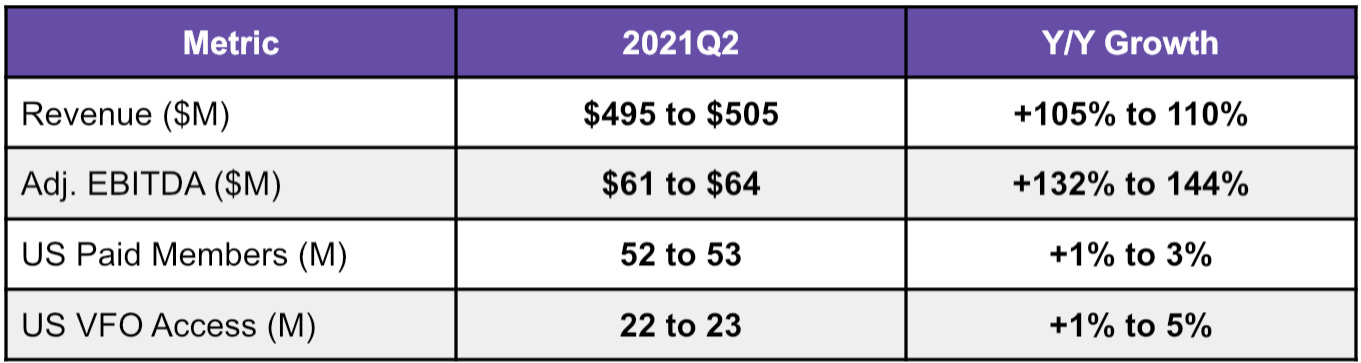

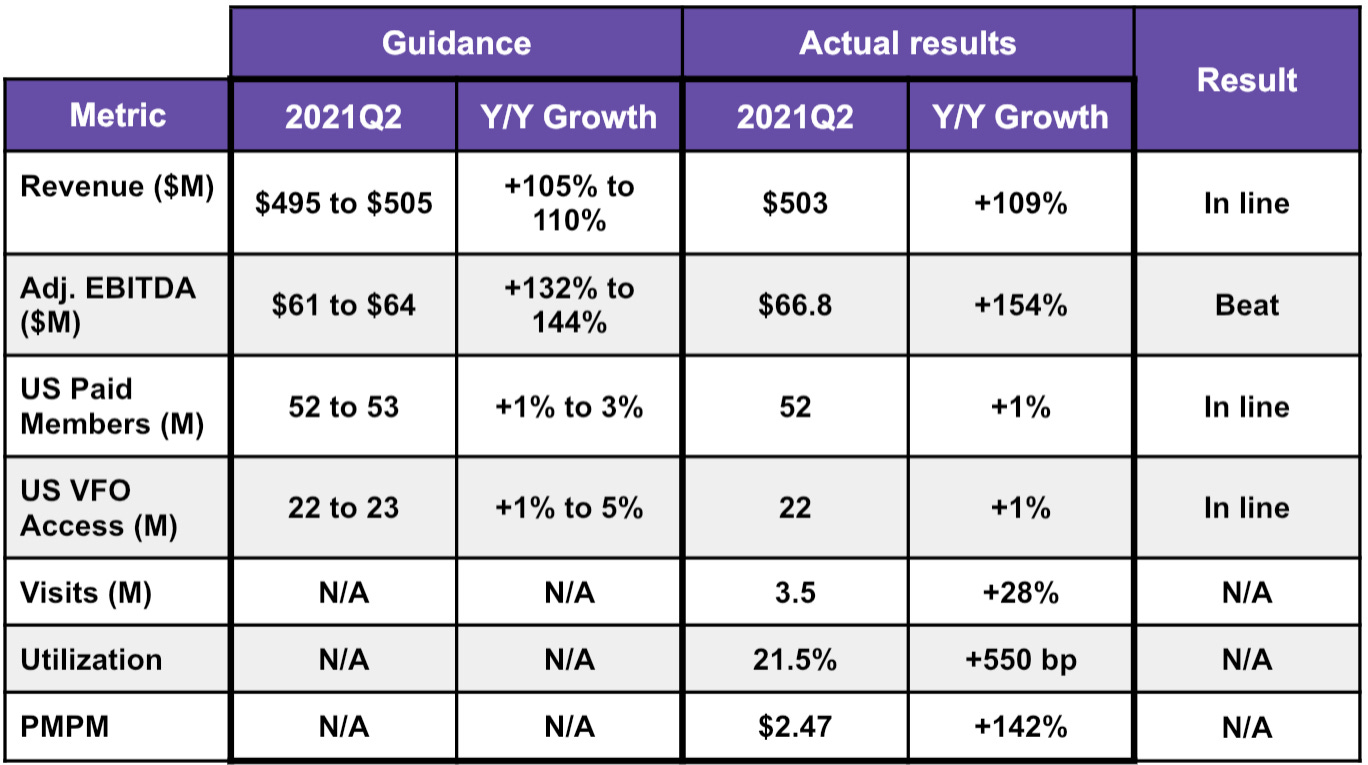

Before digging in the actual quarterly results, let’s take a look at what management had guided for this quarter when it announced the Q1 2021 earnings results three months ago:

There are other key metrics for Teladoc but management only gives guidance on the ones you see in the table above.

If we look solely at the quantitative results, the quarter was in line with management's expectations. Revenue grew 109% Y/Y to $503 million driven primarily by domestic access fee revenue (recurrent) which is increasing as a percentage of total revenue (86% as of 2021 Q2). This trend can be expected to continue in the coming quarters as InTouch and Livongo follow a subscription-based model.

Organic revenue grew 41% Y/Y (organic revenue doesn’t take into account InTouch and Livongo revenue) which is also impressive considering that the comparable quarter is the peak of the first wave of the pandemic where Teladoc saw its revenue increase significantly. This is what you will often see referred to as “tough comps” which stands for “tough comparisons” with the comparable period.

US Paid Members and US Visit Only Access came in at 52 million and 22 million respectively. Although these results were in line with guidance, they came in at the lower end (+1% Y/Y) and some investors were not impressed. As I have said before, this is nothing to worry about in the short term because the pandemic pushed forward a huge amount of member growth which needs to settle. For a little bit of context, members stood at 36.7 million before the pandemic unfolded and increased to 51.5 million in just two quarters! These two metrics have been facing tough comps since the unveiling of the pandemic.

On top of that, there were quite a bit of temporary members, which now fall off and have to be replaced with new members to even stay at the same level. This will only be the case for a few pandemic quarters, though.

Visits came in at 3.5 million or an increase of 28% Y/Y. This might seem low but it is indeed very strong when contextualized. During the first wave of the pandemic, telehealth visits took a giant leap and Teladoc managed to increase visits 28% from those levels. It is even more encouraging when you see that these visits are coming from non-COVID related sources because these are the visits that are sustainable over the long term:

During the second quarter, 80% of member visits in the B2B channel were related to noninfectious diseases versus approximately 50% in the pre-pandemic period.

Teladoc CEO Jason Gorevic on the 2021 Q2 Earnings Call

Turning to profitability, even though the company beat the high estimate of Adjusted EBITDA guidance, posting an impressive increase of 154% Y/Y (13.3% margin), it failed to meet analysts' expectations on GAAP earnings. Teladoc posted net losses of $133.8 million, which is obviously worrying on first sight but not worrying at all over the long term if you analyze where these losses are coming from:

$83 million in stock-based compensation expense related to Livongo stock awards. In fact, Teladoc’s weighted average number of shares doubled with respect to the same quarter last year

$46.1 million of amortization of intangibles coming from Livongo and InTouch acquisitions. Livongo and InTouch had intangible assets such as patents and its trademark. When these intangibles have a useful end date on them, like with patents, then an acquiring company is required to amortize these over time. But this doesn't cost Teladoc anything

$31.4 million loss in the extinguishment of debt, which means that Teladoc has recalled debt. I can only see that as a positive, even though it looks bad in the EPS.

$90.2 million non-cash income tax expense

These expenses make up a total of $250.7 million and they have two things in common: they all are non-recurring or one-time expenses in nature which will eventually go away and they don't cost Teladoc any cash.

Now to assess the product quality and engagement we can look at two main indicators: PMPM and Utilization. PMPM stands for Per Member Per Month. It basically calculates the total healthcare costs for a single member in a month.

PMPM for the second quarter was $2.47, up 142% Y/Y and also up 10.3% Q/Q driven primarily by specialty care (D2C mental health and chronic care) which have a higher PMPM. Further PMPM increases can be expected in the future as the company rolls out Primary360 and comprehensive whole care products. The company is still very early into the PMPM increase.

Utilization, which basically measures member engagement, continued its trend upwards and stood at 21.5%, increasing 550 basis points Y/Y. This metric is expected to increase even further over the long term too as long as the company rolls out more comprehensive whole care products. The logic is straightforward, if I can access one app for all my healthcare needs, both physical and mental, chances are that I will use it constantly.

There was also good news in chronic care enrollment which grew 45% Y/Y to 715k. This is where Teladoc’s advantage lies because it enables the company to roll out whole-care products to an already existing loyal member base while helping the company collect recurring data which will enhance care personalization.

Lastly, I would like to wrap up the numbers part with this graph on gross margins which have significantly improved both on a year over year basis and sequentially:

Here's a summarizing overview of the Q2 numbers:

All in all, these were good quantitative results, in line with expectations, although they were nothing too spectacular in a stock market where many investors focus more on the beats than the actual revenue growth and the long-term opportunities.

Interestingly enough, these results took many investors by surprise which does not make much sense as, during the 2021Q1 Earnings Call, Mala Murthy (Teladoc’s CFO) said that 2021 was going to be an investment year for the company:

The good thing is we have a very, very clear road map. And we have spent a fair amount of time as a leadership team, prioritizing that road map, so that the investments we've put against that, as we have talked about, I expect 2021 to be an investment year, it is stacked and aligned against those very clear priorities in the R&D road map.

Source: 2021Q1 Earnings Call Transcript

This basically means that 2021 will be the year during which management will prepare the company for 2022 and beyond. With this in mind, the background was much more important this quarter than the numbers. There were several things I was particularly interested in going into earnings:

Status of Livongo integration

Primary360 developments and deals

New comprehensive product rollouts

International growth: unfortunately, this one had to wait as the company is still focused on integration and the domestic business

Let’s see what management had to say about these topics.

The Background Information

The call kicked off with two great quotes from CEO Jason Gorevic that clearly demonstrate that the vision of the company is unmatched in the industry:

It’s not enough to simply virtualize the current healthcare experience.

We need a single virtual solution that seamlessly takes care of all of a person’s healthcare needs, redefines the customer experience and uses data to improve care at scale.

Source: 2021Q2 Earnings Call Transcript

The integration of Teladoc and Livongo continues its path. During the last Earnings call (2021 Q1) management said that they had already integrated the sales teams of both companies and the update this quarter is even better. The company launched the first integrated Livongo-Teladoc product: myStrength Complete. This product combines Teladoc’s therapists and psychiatrists with Livongo’s mental coaching capabilities. It's a first taste of the potential synergies of the merger.

The merger between both companies surely is a controversial topic for many investors. Some Livongo investors sold their shares after the merger announcement or during the next couple of quarters, when Livongo was worth $18 billion (the acquisition price) and they have become vocal bears, attacking the combined company, now being worth only $23 billion. They seem to think that Teladoc is eroding Livongo’s business, which is far from true. Teladoc will enable Livongo to increase its reach and Livongo will enable Teladoc to leverage its data pool, AI insights, preventive healthcare, subscription revenue and loyal customer base.

There was more news on the whole-care product front, as Primary360 continues to tick the interest of big players. Teladoc has signed a “significant national agreement” and is in very late-stage discussions with several other big players. As I said in the previous article on the company, this product is the first step towards whole-person care and will be responsible for increased utilization and increased multi-product adoption. These two metrics will be the main drivers of higher PMPM:

The fact that our sales are now 75%-plus multi-product drives higher revenue per member.

Jason Gorevic on the 2021 Q2 Earnings Call

Multi-product adoption is exactly what management is focused on right now. Building a whole-care product that drives multi-product adoption across existing members is much more important than membership growth because members will eventually come to the most complete offering in the market. On the other hand, if management was focused on membership growth without offering a whole-care product then these members would eventually leave.

Primary360 and myStrength are going to bring significant member growth as they gain adoption. For example, the company has signed a new expansive agreement with HCSC, the fifth-largest health insurance company in the US (around 16 million insured), which will enable Teladoc to offer diabetes and hypertension programs for the fully insured plans. This agreement will start at the beginning of 2022 so once again, don’t expect something spectacular for 2021:

We're incredibly excited about the HCSC relationship. In fact, I'd call it a landmark deal for us. We will be rolling out into significant and multiple commercial fully insured markets of theirs. So when you ask what's signed in terms of a contract, we have signed contracts to roll out to those populations. We have good visibility into the revenue that will come from that. And so that is essentially locked and loaded. - Jason Gorevic

From the 2021 Q2 Earnings Call

Another important development is the relationship with Microsoft to integrate Teladoc’s Solo platform for hospitals and health systems directly into Teams. This partnership shows two things:

Players such as Microsoft, Zoom and Webex will try to participate in the revenue that the telehealth space has to offer through their communication services

These players will need Teladoc’s products if they want these dollars

There has been extreme fear, probably driven by negative price action, about the competitive landscape of the telehealth industry and the stigma of commoditization. Teladoc has fallen time and time again on the same fears of Amazon Care and with people arguing that they have no moat because telehealth is just a video call with a doctor.

These fears are clearly overstated. A part of Teladoc's moat is in data advantage which increases together with increased utilization and increased data collection, this is not simply connecting doctors with patients and the Microsoft + Teladoc partnership is again evidence of this.

Another thing that caught my attention was the following question by David Larsen, a BTIG analyst:

Can you talk a little bit about the last mile of care? Do you have any interest or plans in getting into, like, say, the visiting nurse business?

Management has always pointed out that it wanted to deliver whole-care virtually and it wanted to be the first place where any patient goes before entering the physical health system. This question is very interesting because in case the company would be willing to go into this business then it would automatically become a virtual-physical health company which would probably erode its margins. Don’t worry, this is what Jason Gorevic answered:

I would say that's a very important evolving part of the market and one that I want to partner with. I think the likelihood of us owning a field team that's going to be making house calls is pretty small.

In fact, Teladoc is already working on these partnerships for its Primary360 product which is great to know because it even more widens the whole-person-care vision without suffering margin compression.

And last but not least, I would like to touch on a point that I think is quite important but I haven’t seen mentioned elsewhere: the change in reimbursement models over the long term. Going forward, management expects a change in the reimbursement model towards a value-based reimbursement model where Teladoc shares the risk with its clients. The fact that the company is thinking already about these types of models shows high confidence by management in the quality of its products.

You should look out for continued investments in all of these matters (integrated products, new deals, integration…) during the second half of 2021. Management did not give a great level of detail on the deals and the new product launches although they did state several times that investors would have access to more detail during Investor Day which is scheduled to occur during Q4.

The market’s reaction

Let’s take a quick look at Teladoc’s stock price action post earnings. The stock fell sharply after hours and opened down on the day just to recover and end in positive territory:

Judging solely by the market’s reaction one could think that Teladoc’s earnings were poor but what really happened is that the market’s incentives were clearly misaligned with those of the company. The company has said several times that 2021 will be an investment year where significant advances on the integration and product front have to be made to prepare the company for the years ahead. This probably clashed directly with those investors who sold their shares because they thought that 2021 would be a year of significant stock returns.

If you decide to invest, you should always know what you own and for how long you plan to hold it for. My investment horizon in Teladoc, and in all of my holdings, is +5 years so I am very comfortable holding it even if it trades sideways for a while. Those investors who think that they can jump out now and hop back in when share price starts to move may find out the hard way that the market can’t be timed that easily. The bear case has shifted from “Intense competition” to “Opportunity Cost”.

This is why I always hold and never sell as long as the thesis is intact. You can never know what the market will do over the short term. Can Teladoc go to $200 in two months? Why not? Can Teladoc go to $100 in two months? Why not? Don’t focus on predicting stock movements when you can focus on analyzing the business.

You should also take into account that Teladoc’s management is not that great at marketing the results which also plays an important role in short-term movements. For example, PMPM, one of the main drivers of long-term revenue, increased 142% Y/Y but management never gave this percentage increase during the call.

Conclusion

Teladoc’s numbers were good although not outstanding. That was to be expected during this investment year. The background information, however, made clear that the company’s products continue to gain traction in the market and management is entirely focused on preparing the company for the long term.

With this in mind, I think that Teladoc will be a very rewarding investment for those patient investors who understand the business and can abstract from price action to focus on fundamentals.

Pinterest (PINS) also reported results that same week and, even though I will not be writing an article on it, I posted a thread on Twitter with my thoughts about the ER:

Stay well!

IQ

If you liked this article don’t forget to subscribe to receive notifications when future articles are published!

Hi IQ,

Thanks for your analysis and write-up. Much appreciated. I am also holding TDOC based on a few key reasons that you highlighted such as increasing trend of PMPM and ability to go higher with the integration of products, Jason's vision and passion, digital disruption on the industry with increasing TAM, and advantage of data analytics as a first mover advantage.

However, I also appreciate the limitation of the land strategy and shifting their focus more on expand. Jason commented in the call about 70 million people who currently have access to TDOC service, and knowing that US employment number is about 160-170M, TDOC is at ~42% market penetration. Hence, I agree with you that it is important to monitor their ability to launch new products (must be sticky), cross sell them and the ability to execute. Something like CRWD.